ESG Reporting Monitor Switzerland 2025 From Small Caps to Large Caps: Sustainability Reporting Under Voluntary International Standards

Executive Summary

| In 2025, ESG reporting is undergoing a transformation: While regulatory requirements in Europe are increasing significantly, other countries – most notably the United States – are pursuing the opposite course. International companies are thus faced with the challenge of responding to divergent political signals, investor demands and societal expectations. In particular, the regulatory framework in Europe is becoming increasingly stringent. It is becoming more and more challenging for companies to keep track of new reporting obligations, audit requirements and standards – a development that also affects Switzerland. National legislation is being aligned with European standards, bringing a significantly larger number of companies into scope and increasing transparency and governance requirements. Against this backdrop, this year’s analysis of sustainability reports from companies listed in the SMI Expanded and SPI Extra reveals a high level of activity, while also showing notable differences: 93% of the companies surveyed already publish a sustainability report, but the breadth and depth of reporting vary considerably. Compared with the previous year, companies in the SMI Expanded are, on average, making less use of voluntary standards. In particular, SASB, UNGC, SDGs and CDP show noticeable declines. The trend appears to be moving towards a more selective approach rather than maximum coverage, possibly as a response to increasing regulatory overload. Smaller and medium-sized companies (SPI Extra) are generally showing growing interest in ESG standards but continue to lag significantly behind the blue chips in terms of depth and variety of application. There is also a growing trend towards stronger integration of sustainability into the annual report: 64% of SMI companies opt for an integrated presentation, and 81% have their report fully or partially externally audited. As a result, ESG reporting is gradually evolving from a mere compliance exercise into a strategic instrument that not only fosters transparency but also contributes to credible market positioning. Those who use sustainability reporting in a targeted manner today strengthen not only their regulatory resilience but also the trust of investors, customers and employees. |

|---|

Changing Landscape in Sustainability Reporting

Between Regulation, Resistance and Transformation

In 2025, sustainability reporting will find itself in a paradoxical situation: advancing in terms of regulation, under political pressure and socially debated.

While the European Union has introduced the most comprehensive standards for ESG transparency to date through the Corporate Sustainability Reporting Directive (CSRD) and the European Sustainability Reporting Standards (ESRS), a noticeably different wind is blowing from other regions of the world – most notably the United States: political backlash, deregulation, and growing criticism of ESG. The Trump administration has triggered a cooling towards sustainability agendas, climate targets and diversity initiatives.

This change of course has led many US companies to roll back ESG initiatives, ease reporting obligations, and refrain from making public commitments to climate strategies. ESG is increasingly politicised and, in conservative circles, attacked as a symbol of ideologically driven regulation.

At the same time, the opposite is true in Europe: the CSRD is fully in force, and the first companies are already reporting in accordance with the new requirements. This widens the gap between the two worlds and raises the question: how do internationally active companies position themselves in this growing divide?

In many boardrooms in 2025, a mix of regulatory obligation, strategic recognition and ESG fatigue prevails. But the facts are clear: anyone doing business in or with Europe will have no choice but to comply with the new obligations.

Since 2024, the CSRD has required large EU companies to provide comprehensive ESG reporting, and from the 2025 financial year onwards, it also applies to many listed SMEs. The thresholds are low (any two of the following: 250 employees, €40 million turnover, €20 million balance sheet total), affecting around 60,000 companies.

One of the key changes introduced by the CSRD is that companies must report more comprehensively and according to standardised criteria. Moreover, sustainability information must be an integral part of the management report, and subject to external assurance. This clearly shows that sustainability reporting is gradually being brought into line with traditional financial reporting. The CSRD also enshrines the principle of double materiality, which requires companies to report both on the impact of their business activities on people and the environment (‘impact materiality’, inside-out perspective) and on the financial effects of sustainability-related factors on the company (‘financial materiality’, outside-in perspective).

For many companies, especially small and medium-sized enterprises, these requirements present a significant challenge. The complexity of the content, the breadth of reporting requirements, and limited internal resources make implementation demanding. The wide range of cross-sector and industry-specific standards, formatting rules, audit obligations and digital disclosure requirements means many companies rely on external support.

The CSRD is complemented by the EU Taxonomy and the Sustainable Finance Disclosure Regulation (SFDR) – a tightly interwoven regulatory framework that primarily affects large, capital-market-oriented or internationally active companies, but is increasingly drawing in smaller players too.

Switzerland Under Pressure to Align with EU ESG Rules

Switzerland has also gradually tightened its ESG legislation. Since 1 January 2022, new regulations under the Swiss Code of Obligations (Articles 964a–c CO) have applied. Currently, publicly listed companies, banks and insurance providers must report on climate-related matters if they exceed two of the following thresholds for two consecutive financial years: 500 employees, CHF 40 million in turnover, or CHF 20 million in total assets. They are required to report annually on:

- Environment, social issues, labour rights, human rights and anti-corruption

- Climate risks in accordance with the TCFD (including governance, strategy and metrics)

- Due diligence and reporting obligations regarding conflict minerals and child labour

In spring 2025, a consultation process to expand the reporting obligation was completed, and a draft bill is in development. The aim is to lower the thresholds to 250 employees, CHF 40 million in turnover, or CHF 25 million in total assets, aligning with the EU. As a result, around 3,500 companies in Switzerland would become subject to reporting requirements, compared to just 300 currently.

Global Divergence – and Its Strategic Implications

For internationally active companies, this divergence presents a strategic challenge. Those operating both in Switzerland or the EU and in deregulated markets like the United States must navigate varying expectations, political signals and investor demands.

Yet even in less regulated markets, ESG remains relevant – not due to political mandates, but due to market pressure, reputational risks and capital requirements. Many institutional investors still expect robust sustainability data.

In 2025, sustainability reporting is no longer driven by idealism, but by realism. It is regulated, comparable, auditable – and indispensable for companies seeking to build trust, secure capital and succeed over the long term.

The Most Common Standards and Their Prevalence in the SMI Expanded and SPI Extra

This study analysed all sustainability reports published by 31 May 2025 from companies listed in the Swiss equity indices SMI Expanded and SPI Extra, to provide a comprehensive overview of sustainability reporting for the 2024 financial year. The SMI Expanded includes the 50 largest Swiss companies by market capitalisation, while the SPI Extra comprises small and mid-cap companies that are not listed in the SMI.

Out of the 190 companies analysed, 176 (93%) either dedicate a substantial section of their annual report to sustainability or publish a standalone sustainability report. The 14 companies that did not publish a report are all part of the SPI Extra, making them a clear minority. For eight companies, the 2023 report was included, as their 2024 reports had not yet been published by the cut-off date.

The following section introduces the six most commonly used voluntary standards and frameworks for sustainability reporting and analyses how they are applied by companies in the SMI Expanded and SPI Extra. This is supplemented by a look back at developments in recent years – with a direct comparison to previous IRF studies on sustainability reporting by SMI Expanded companies in 2024, 2023 and 2021.

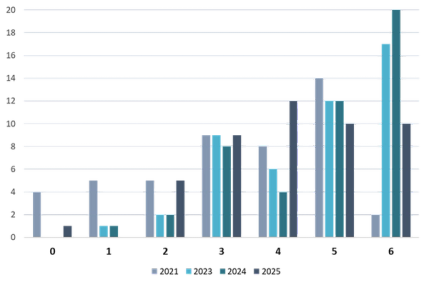

Among the 47 SMI Expanded companies, a high level of engagement remains evident: more than two-thirds (68%) apply at least four standards, with ten companies incorporating all six frameworks examined. Only one company refrains entirely from using voluntary standards – an exception in the otherwise highly standardised environment of large-cap companies.

Compared with previous years, the overall level of standard adoption in the SMI Expanded remains high, though a noticeable shift in distribution is emerging. While 43% of companies applied all six standards in 2024 – the highest proportion to date – this share dropped significantly in 2025. At the same time, the use of four standards increased considerably, suggesting that companies are narrowing their focus and now prioritising more deliberately which frameworks are strategically relevant. The long-term development since 2021 is shown in Figure 1.

Figure 1: Number of voluntary standards applied by companies in the SMI Expanded

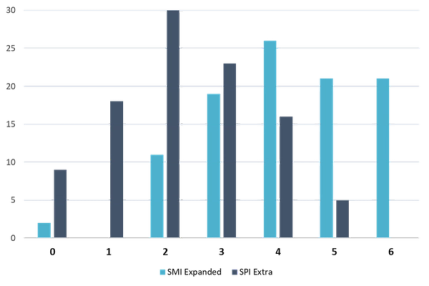

The picture is quite different among the 129 companies in the SPI Extra that publish a sustainability report. In 2025, only around 20% apply four or more standards, while more than half (57%) apply just one or two – or none at all. Twelve companies did not apply any voluntary standard.

This comparison (see Figure 2) makes one thing clear: while sustainability reporting has become a firmly established part of corporate strategy in the SMI Expanded, many small and mid-sized companies are still in the process of building relevant structures – or are reporting primarily to meet minimum legal requirements.

Figure 2: Distribution of applied standards among companies in the SMI Expanded & SPI Extra (in percent)

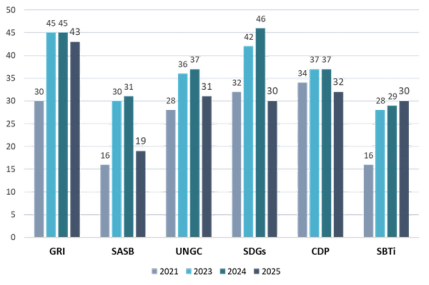

Figure 3: Number of SMI Expanded companies reporting according to each standard

Global Reporting Initiative (GRI)

The standards by the Global Reporting Initiative (GRI) are the most widely used sustainability reporting standards worldwide. They support companies in understanding and disclosing their economic, environmental, and social impacts. The GRI standards cover a broad range of topics, including environmental effects, human rights, and supply chain management. They are categorised into GRI Universal Standards for all organisations, GRI Sector Standards for specific industries, and GRI Topic Standards for particular topics.

At the end of 2021, the GRI standards were comprehensively updated, affecting reporting options. Previously, companies could choose between the options “Core”, “Comprehensive”, and “Referenced”. With the new standards, companies report either “in accordance with GRI” or “with reference to GRI”. In the first approach, companies report comprehensively on all material topics and the associated impacts as well as how they deal with these topics. Companies that are unable to meet some of the requirements of the GRI Standards or only wish to report certain information can choose the second approach.

In the 2025 reporting year, 43 of the 47 companies in the SMI Expanded (91%) based their sustainability reporting on the GRI standards. Of these, 26 reported in accordance with the standards, while 17 used referencing. This means GRI adoption in the SMI Expanded remains nearly universal and has remained stable over recent years: 45 companies used the GRI Standards in both 2023 and 2024, compared to 30 in 2021.

In the SPI Extra, GRI usage is also notable: of the 129 small and mid-cap companies publishing a sustainability report, 103 (80%) applied the GRI Standards – 69 in accordance, and 34 using the referencing option.

Sustainability Accounting Standards Board (SASB)

The Sustainability Accounting Standards Board (SASB) provides industry-specific frameworks for disclosing financially material sustainability information. The standards help companies identify, manage, and communicate ESG issues that are particularly relevant to financial performance in their sector. The aim is to complement traditional financial reporting with essential sustainability-related disclosures – for example, climate risks and their potential business impact. Since August 2022, the SASB Standards have been maintained and further developed by the International Sustainability Standards Board (ISSB) under the IFRS Foundation.

In 2025, 19 of the 47 SMI Expanded companies (around 40%) integrated the SASB Standards into their sustainability reports. This marks a noticeable decline for the first time in several years: 31 companies applied the standards in 2024, and 30 in 2023. Adoption had previously grown steadily from just 16 companies in 2021.

In the SPI Extra, the SASB Standards play a minimal role. Of the 129 companies examined, only four (3%) reported using the standards in their sustainability reports. A few additional companies referenced the SASB framework in their materiality analysis, but did not apply the standards systematically.

Many companies combine GRI and SASB in their reporting, often presenting them together in a consolidated index. This dual application has proven effective, as the two frameworks offer complementary perspectives: SASB focuses on financially material ESG topics from an investor's perspective (“financial materiality”), while GRI provides a broader view of a company’s impact on society and the environment (“impact materiality”).

UN Global Compact (UNGC)

The UN Global Compact is an initiative launched by the United Nations to encourage companies to adopt sustainable and socially responsible business practices. By joining, companies commit to ten universally recognized principles in the areas of human rights, labor, environment, and anti-corruption, and they pledge to report regularly on their progress. Around 25,000 companies and organisations from 167 countries worldwide have now signed up to the UN Global Compact.

According to the UNGC’s online database, 31 of the 47 SMI Expanded companies (66%) have signed the UN Global Compact. By doing so, they have not only committed themselves to the principles of the UNGC, but also to submitting an annual progress report. This demonstrates an ongoing commitment to the UNGC principles at the board and/or management level. In previous years, 37 companies had signed in 2024, 36 in 2023, and 28 in 2021, indicating a slight decline compared to earlier years.

Among SPI Extra companies, the UN Global Compact is also represented: 34 of the 129 companies (26%) with a sustainability report have joined the initiative. This suggests that smaller companies are also taking on responsibility within international frameworks – though at a significantly lower rate than their mid- and large-cap peers in the SMI Expanded.

Sustainable Development Goals (SDGs)

The 17 Sustainable Development Goals (SDGs) are targets for global sustainable development set by the United Nations in 2015 as part of the 2030 Agenda. The SDGs encompass all three dimensions of sustainability (environmental, social, and governance) and cover topics such as poverty alleviation, gender equality, and environmental protection.

Although originally not intended as a framework for sustainability reporting, the SDGs now provide companies with a good reference for defining their sustainability goals, setting priorities, as well as measuring and communicating progress. To help companies integrate the SDGs into their sustainability reporting, the UN Global Compact, GRI, and World Business Council for Sustainable Development (WBCSD) developed the SDG Compass.

Today, the SDGs are firmly established in the sustainability reporting of many Swiss companies. In 2025, 40 of the 47 SMI Expanded companies (85%) included the SDGs in their reports. However, this marks a noticeable decline from the previous year (46 companies in 2024) and 2023 (42 companies) – making 2025 the first year since 2021 (32 companies) without further growth. While SDG coverage remains high overall, the decline suggests that some companies are reassessing their reporting approach or shifting focus to other frameworks.

Of the companies continuing to apply the SDGs, 38 also use the GRI Standards (95%) and 25 (63%) additionally incorporate the UN Global Compact, highlighting how the SDGs remain embedded within broader reporting structures.

In the SPI Extra, 88 of the 129 companies (68%) with sustainability reports integrated the SDGs into their reporting. Most of these (78 companies or 89%) combined them with GRI. Twenty-three companies (26%) went further, also including the UNGC principles. Compared with the SMI Expanded, this indicates a general interest in the SDGs among smaller companies, albeit with lower prevalence and depth of integration.

CO2 Reporting

A central component of sustainability reporting is the disclosure of company-related CO? emissions. The most widely used and recognised international framework for the measurement and reporting of greenhouse gas emissions is the Greenhouse Gas Protocol (GHG Protocol). It offers companies a standardised approach to emissions measurement, providing the foundation for comparability, transparency and credibility. The GHG Protocol divides a company’s emissions into three categories: Scope 1 includes direct emissions from company-owned sources, Scope 2 refers to indirect emissions from purchased energy, and Scope 3 covers all other indirect emissions along the upstream and downstream value chain. The following standards relate to measurements in accordance with the GHG Protocol.

Carbon Disclosure Project (CDP)

The Carbon Disclosure Project (CDP) is an internationally active non-profit organisation that supports companies in systematically recording, managing and transparently reporting their greenhouse gas emissions. Once a year, companies are invited to disclose information on their emissions, climate strategies and other environmental topics via standardised questionnaires. The submitted data is collected and assessed in a publicly accessible online database.

With around 22,700 companies assessed in 2024, CDP is the world’s largest environmental database. Assessment is carried out in the areas of climate, forests and water, with scores ranging from A (best score) to D. Companies that do not provide sufficient information or do not complete the questionnaire are rated F. For this study, CDP ratings in the climate category from A to D were considered.

In 2025, 32 of the 47 companies examined from the SMI Expanded (68%) completed the CDP climate questionnaire sufficiently. Participation is therefore noticeably lower than in the previous two years: both in 2023 and 2024, 37 companies took part. Of the 32 reporting companies in the current year, 22 were rated A or B, six were rated C and four received a D rating.

In the SPI Extra, participation is significantly lower: 40 of the 129 companies (31%) that publish a sustainability report completed the CDP questionnaire in full. The ratings vary: 20 of these companies were rated A or B, ten received a C and ten a D.

Science Based Targets initiative (SBTi)

The Science Based Targets initiative (SBTi) is a global partnership between CDP, the UN Global Compact, the World Resources Institute (WRI) and WWF. It supports companies in setting science-based targets to reduce their greenhouse gas emissions – in line with the Paris Agreement and the goal of limiting global warming to 1.5°C. With the Net-Zero Standard introduced in October 2021, the SBTi also offers companies a clearly defined, science-based framework for long-term climate strategies, including the achievement of net-zero emissions.

An online database maintained by the SBTi lists companies that have already set science-based targets or have committed to developing them within 24 months. According to current data (as of June 2025), around 10,700 companies worldwide have either set science-based emission reduction targets or have committed to doing so. Around 8,000 companies already have validated targets and around 1,800 companies have formulated net-zero targets. SBTi is thus regarded as an internationally recognised reference framework for credible climate targets and is gaining increasing importance among investors, regulators and rating agencies.

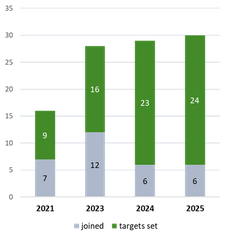

In 2025, 30 of the 47 companies examined from the SMI Expanded (64%) were listed in the SBTi database. Of these, 24 had already published validated, science-based emission reduction targets, while six had joined the initiative and are currently developing such targets. Unlike other frameworks examined, the number of companies listed in the SBTi from the SMI Expanded has not declined: after 16 companies in 2021, and 28 and 29 in 2023 and 2024 respectively, there is a slight increase in 2025.

In the SPI Extra, participation in the SBTi is significantly lower: 29 of the 129 companies (22%) that publish a sustainability report are listed in the database. Of these, 16 have already set science-based climate targets, while 13 have committed to developing targets. Notably, two companies have withdrawn their near-term and net-zero targets – a rare but notable step in the dynamic field of climate reporting.

Figure 4: Number of SMI Expanded companies that have joined the SBTi or already

set emissions reduction targets under the SBTi

Sustainability in the Right Format

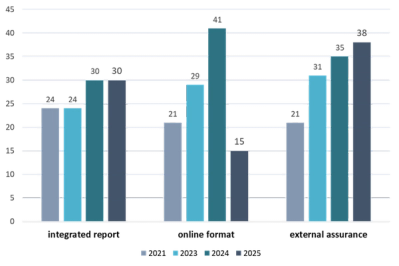

In 2025, many companies once again opted for integrated sustainability reporting. 30 of the 47 analysed companies in the SMI Expanded (64%) incorporated their sustainability report into the annual report – the same number as in the previous year. This form of reporting allows financial and non-financial information to be combined in a single document, thereby supporting a holistic assessment of corporate performance. It therefore remains widely established. By comparison: in both 2023 and 2021, 24 companies chose this reporting format.

Online publication shows lower figures in the current year, which is due to a methodological adjustment. Only reports that were published entirely online, in addition to being available as a PDF download, were considered. This format offers several advantages, including the ability to link content via hyperlinks, interactive elements, and improved search engine visibility. Sustainability reports that were only partially available online were not included, as a clear distinction has become increasingly difficult. Based on this definition, 15 companies in the SMI Expanded (32%) presented their report fully online. In previous years, under a broader definition, the figures were significantly higher: 41 in 2024, 29 in 2023, and 21 in 2021.

External assurance of sustainability information continues to gain importance. 38 companies in the SMI Expanded (81%) had their report fully or partially audited by an independent body – more than in previous years (35 in 2024, 31 in 2023, and 21 in 2021). This highlights the growing expectations regarding transparency, reliability, and data quality.

Companies in the SPI Extra are also approaching this level. 70 of the 129 analysed small and mid-cap companies (54%) that publish a sustainability report integrated it into their annual report. 33 (26%) presented it fully online, and 49 (38%) subjected it to external assurance. This demonstrates that smaller companies are also placing increasing emphasis on professionalism and transparency in their sustainability communications.

Figure 5: Number of SMI Expanded companies with integrated reporting, online format (fully online from 2025),

and external assurance

Recommendations for Swiss Companies

- Select standards strategically rather than aiming for maximum coverage. Not every framework is equally relevant for every company. The choice should be guided by sector, company size, market environment, and target audiences.

- Use combinations consciously. A well-balanced mix of GRI (structure), SDGs (goals), and UNGC (values) creates a robust and coherent communication framework. SASB, CDP, and SBTi add further depth, particularly in relation to investors and climate relevance.

- Understand double materiality – don’t just comply. The CSRD requires more than data collection. Companies should actively engage with their impacts and risks and communicate them in a clear and transparent manner.

- Plan external assurance strategically. Third-party verification not only improves data quality but also enhances credibility with investors and the public.

- View reports as strategic communication tools. Transparent, clear and credible ESG communication strengthens not only reputation, but also resilience in the market.

- Don’t wait for regulatory pressure. Companies below the legal reporting thresholds can also benefit from a clear ESG positioning – in terms of competitiveness, access to capital, and employer branding.

Which ESG Standard Suits Which Type of Company?

| Standard | Typical Areas of Application | Purpose and Benefits | Recommendation for Corporate Communication |

|---|---|---|---|

| GRI | Companies of all sizes and industries – especially as an entry point and base standard | Comprehensive coverage of all ESG topics; high international acceptance; good comparability | Ideal as a structural foundation |

| SASB | Capital market-oriented companies with industry-specific ESG risk exposure | Financial materiality; investor relevance; complements traditional financial reporting | Ideal in combination with GRI; particularly relevant for listed companies |

| UNGC | Companies with international presence & CSR commitment | Values- and principles-based positioning; internationally compatible | Communicatively effective; easy to implement; enhances reputation and trust |

| SDGs | Companies with societal impact & sustainability strategy | Narrative anchoring of sustainability | Useful for storytelling & visualisation – but not sufficient on their own |

| CDP | Companies with significant environmental exposure or investor focus | Internationale Benchmarking-Plattform; relevante Kennzahlen zu Klimastrategien und Emissionen | International benchmarking platform; key climate strategy and emissions metrics |

| SBTi | Companies with ambitious climate targets or ESG leadership ambition | Science-based emission targets; high credibility | Strategically valuable for credible positioning; sets clear standards but requires resources and commitment |

About IRF

In recent years, IRF has established itself as one of the leading Swiss consulting firms for economic issues. IRF counts around 40 Swiss and international companies among its regular clients. In addition, IRF has made a name for itself in crisis communication and in accompanying capital market transactions.

Contact

Laura Berkes, Consultant

+41 43 244 81 44