Sustainability Reporting of the Largest Listed Swiss Companies According to International Standards

Executive Summary

In recent years, sustainability reporting has gained significant importance. Companies are increasingly in the spotlight of the global society, which demands more comprehensive and detailed reports on their ecological and social impacts. Transparent sustainability reporting not only strengthens a company’s reputation but also creates significant competitive advantages, increases trust, and promotes long-term success.

In the EU, companies must navigate an increasingly complex landscape of regulatory requirements. The Corporate Sustainability Reporting Directive (CSRD) in particular entails more comprehensive reporting obligations to ensure more transparent and standardized reporting. Switzerland has also introduced stricter regulations, closely aligned with EU directives, though their implementation still raises questions.

In addition to regulatory requirements, voluntary sustainability standards and guidelines play a significant role in sustainability reporting. This study provides an overview of the key standards and illustrates their adoption among the largest listed companies in Switzerland, as measured by the SMI Expanded Index. The majority of the 47 companies analyzed applied five or all six of the examined standards. The most widely adopted standards remain those of the Global Reporting Initiative (GRI), the UN Global Compact (UNGC), and the Carbon Disclosure Project (CDP). With one exception, all companies align with the 17 Sustainable Development Goals (SDGs) of the United Nations. Additionally, an increasing number of companies are setting clear emission reduction targets as part of the Science Based Targets initiative (SBTi).

About two-thirds of the companies integrate their sustainability report into their annual report, with online formats gaining popularity. Moreover, more companies are having their sustainability reports externally audited, indicating a professionalization of the reporting process.

The aim of this study is to provide a comprehensive overview of the current state of sustainability reporting in Switzerland and to highlight how companies are meeting the increased requirements. It is intended to serve as a guide for companies to identify relevant sustainability standards for their specific needs.

Sustainability Reporting in Focus: From Lip Service to Commitment

The urgency of sustainable action has profoundly changed our society in recent years. Companies are no longer only in the spotlight of the markets but also the global community, which increasingly demands that economic success should not come at the expense of the environment and society. Climate change, resource scarcity, and social inequalities are not just issues only for activists and governments – they have become central challenges influencing the strategic direction and daily operations of companies worldwide. The question is not anymore whether a company should act sustainably, but how convincingly it does so and reports on it.

In this context, corporate sustainability reporting has taken on a central role. It serves not only as a means of self-commitment and transparency but also as a strategic tool that helps companies minimize risks and maximize opportunities. Investors, customers, employees, and other stakeholders demand not just empty words but tangible and reliable information about the environmental and social impacts and corresponding measures taken by companies. Transparent reporting not only strengthens a company’s reputation but also creates significant competitive advantages and promotes long-term success. But it is about far more than just economic benefits – it is about being perceived as a responsible actor in a rapidly changing world.

Beyond Compliance

In this dynamic and challenging environment, voluntary reporting standards play a key role. Recognized standards such as those of the Global Reporting Initiative (GRI), the ten principles of the UN Global Compact, and the United Nations’ Sustainable Development Goals (SDGs) provide companies with comprehensive guidelines for the preparation of sustainability reports. These standards enable companies to measure their environmental and social progress, respond to future challenges, and plan appropriate measures. By applying these standards, companies can demonstrate that they not only comply with legal requirements but also actively work towards sustainable and responsible business practices.

However, companies must also navigate an increasingly complex landscape of regulatory requirements. These regulations also play a role in shaping sustainability reporting and set clear expectations for companies. The following summarizes the key regulatory requirements in the EU and Switzerland to provide a comprehensive picture of current requirements and developments in sustainability reporting.

EU Regulations Set Clear Rules

In 2019, the European Union’s (EU) Green Deal laid the foundation for sustainability reporting, with the goal of achieving climate neutrality by 2050 and reducing CO2 emissions by 55% by 2030. To support these ambitious goals, the EU has introduced comprehensive sustainability reporting regulations. In order to avoid greenwashing and create transparency, the EU Taxonomy came into force in January 2022. It classifies sustainable and non-sustainable economic activities across the EU and requires large companies (with more than 500 employees and those selling financial products in the EU) to report on sustainability. Complementary to the EU Taxonomy, various regulations apply at EU level. Since the beginning of 2022, the Sustainable Finance Disclosure Regulation (SFDR) requires EU financial institutions to disclose the weighting of ESG factors (Environmental, Social, and Governance) for their products and cover the entire supply chain in their reporting.

The Corporate Sustainability Reporting Directive (CSRD), which came into force in January 2023, replaces the previous Non-Financial Reporting Directive (NFRD). In addition to intensifying the reporting obligations, the CSRD requires greater transparency and comparability as well as digital documentation. Starting in 2026 (or the 2025 financial year), the CSRD requires not only large but also small and medium-sized publicly listed companies to report if they exceed at least two of the following three amounts in two consecutive financial years: 250 employees, sales revenue of EUR 40 million, or a balance sheet total of EUR 20 million.

One of the key innovations of the CSRD is that companies must report more comprehensively and according to more standardized criteria. Additionally, sustainability information has to be an integral part of the management report and sustainability reporting has to be audited externally. This clearly shows the gradual alignment of sustainability reporting with traditional financial reporting. The CSRD also embeds the principle of double materiality, which requires companies to report both on the impact of their business activities on people and the environment (so-called Impact Materiality, inside-out perspective) and on the impact of sustainability aspects on the company itself (so-called Financial Materiality, outside-in perspective).

The European Sustainability Reporting Standards (ESRS), which were developed by the European Financial Reporting Advisory Group (EFRAG), specify the disclosure requirements under the CSRD. The EU Taxonomy acts as a link between the CSRD and the SFDR. Together, these regulations provide a comprehensive regulatory framework for sustainability reporting in the EU.

New Reporting Requirements for Swiss Companies

Switzerland has also committed to reducing its CO2 emissions by 50% by 2030 compared to 1990 levels by ratifying the Paris Climate Agreement. To this end, large Swiss companies have been required since January 2022 to report on the risks of their business activities in the areas of environment, social, labor, human rights, and anti-corruption, and the measures taken against these risks according to the Swiss Code of Obligations (OR). Additionally, articles 964a to 964c of the OR (“Ordinance on Climate Disclosures”) came into force in January 2023, implementing the latest Federal Council provisions on non-financial reporting.

The new ordinance requires publicly traded companies, banks, and insurance companies to publicly report on climate matters if they exceed at least two of the following three amounts in two consecutive financial years: 500 employees, sales revenue of CHF 40 million, or a balance sheet total of CHF 20 million. It requires detailed reporting in accordance with the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD), which covers the areas of governance, strategy, risk management, as well as key figures and targets. However, the Federal Council does not declare the TCFD recommendations mandatory and allows for flexibility. Alternatively, companies can use other standards to fulfill their reporting obligation on climate matters. While the TCFD covers financial materiality, for example, the European Sustainability Reporting Standards (ESRS) take into account the double materiality requirement specified in the new Swiss ordinance. On the other hand, companies can also cover both perspectives by combining two frameworks (such as GRI and SASB).

Additionally, there are new due diligence and reporting obligations for companies based in Switzerland that import or process minerals or metals containing tin, tantalum, tungsten, or gold from conflict-affected and high-risk areas (so-called conflict minerals). These obligations also apply to companies where there is a reasonable suspicion that their products or services were produced or provided using child labour. Compliance with the Due Diligence and Reporting Obligations in relation to Minerals and Metals must be externally audited, while the auditing of general non-financial reporting and compliance with Due Diligence and Reporting Obligations in relation to Child Labour remains voluntary. The sustainability report must also be approved by the board of directors and the general meeting.

European Winds Drive Switzerland Forward

The new regulations are heavily influenced by EU directives, but their concrete implementation leaves questions unanswered. Sustainability reports from Swiss companies still vary greatly in scope and content, also because the Swiss Code of Obligations has not yet prescribed a fixed reporting standard. While Swiss companies are not directly affected by EU regulations, some are indirectly affected through EU subsidiaries and international and/or cross-border activities. In late June 2024, the Federal Council opened a consultation for changes to the OR, proposing an adapted reporting obligation for companies with 250 employees, sales revenue of CHF 40 million, or a balance sheet total of CHF 25 million (if they exceed at least two of the three amounts in two consecutive financial years). This lowering of thresholds would make about 3,500 companies in Switzerland subject to reporting requirements, up from around 300 currently. Additionally, the sustainability report must be audited by an external auditing company or a conformity assessment body. The choice of reporting standard, however, remains open. Since EU regulations are often adopted in Switzerland sooner or later, it is advisable for Swiss companies to align with EU guidelines.

The Most Common Standards and Their Prevalence in the SMI Expanded

For this study, the sustainability reports of the SMI Expanded companies for the 2023 financial year, published by May 31, 2024, were evaluated. The SMI Expanded comprises the 50 highest-capitalised titles on the Swiss stock market. All 47 companies examined either dedicate an extensive chapter to the topic of sustainability in their annual report or publish a standalone sustainability report. For one company, the 2022 financial year report was taken into account as their 2023 report had not yet been published by the cutoff date. The following presents the most common voluntary standards and guidelines for sustainability reporting and analyzes their practical application within the SMI Expanded companies. Additionally, the results are compared with the findings of the last two IRF studies on the sustainability reporting of SMI Expanded companies from 2023 and 2021.

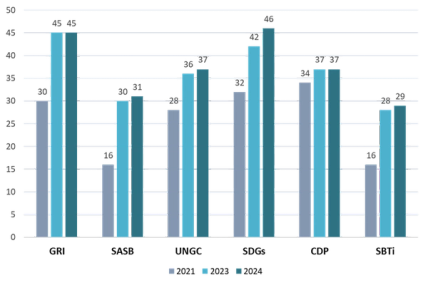

While only a few of the 47 companies examined applied just one (1) or two (2) standards, slightly more companies chose to implement three (8) or four (4) standards. However, the majority of companies applied five (12) or all six (20) of the standards examined. For comparison, in the previous year, 17 companies chose to implement all six standards. In 2021, only two companies applied all six standards. This development clearly indicates that sustainability is no longer a marginal issue but is firmly anchored in corporate strategies.

Number of SMI Expanded companies reporting according to the respective standard

Global Reporting Initiative (GRI)

The standards by the Global Reporting Initiative (GRI) are the most widely used standards for sustainability reporting worldwide. They help companies understand and disclose their economic, environmental, and social impacts. The GRI standards cover a wide range of topics, including environmental impacts, human rights, and supply chain management. They are categorized into GRI Universal Standards for all organizations, GRI Sector Standards for specific industries, and GRI Topic Standards for particular topics.

At the end of 2021, the GRI standards were comprehensively updated, affecting reporting options. Previously, companies could choose between the options “Core”, “Comprehensive”, and “Referenced”. With the new standards, companies report either “in accordance with GRI” or “with reference to GRI”. In the first approach, companies report comprehensively on all material topics and the associated impacts as well as how they deal with these topics. Companies that are unable to meet some of the requirements of the GRI Standards or only wish to report certain information can choose the second approach.

As in the previous year, 45 of the 47 companies examined prepared their sustainability reports according to GRI standards. Of these, 15 reported with reference to GRI and 30 in accordance with GRI. In 2023, 32 companies chose to report in accordance with GRI standards, compared to 27 companies using the “Core” or “Comprehensive” options in 2021. These results illustrate the widespread adoption of GRI standards among the companies analyzed in recent years.

Sustainability Accounting Standards Board (SASB)

The standards of the Sustainability Accounting Standards Board (SASB) also provide a framework for companies to disclose sustainability information. Depending on the industry, financially relevant sustainability information can be identified, managed, and communicated. The standards aim to advance financial reporting by incorporating environmental risks and their potential impacts on the company.

Of the 47 companies examined, 31 have integrated the SASB standards into their sustainability reports. However, only six of these 31 companies are listed in the SASB online database. While the Sustainability Accounting Standards Board claims to monitor the application of SASB standards, they do not collect reported information. To be included in the database, companies must actively prove the application of the standards in their reporting. Although this is voluntary, it is noteworthy that in the previous year, all 30 companies that reported according to SASB standards were listed in the database. In 2021, a total of 15 companies reported according to SASB standards. Therefore, the use of the standards has increased, but many companies no longer seek official confirmation.

Many companies report according to both SASB and GRI standards, combining them in a single report. This combination works well due to the complementarity of the two standards: while SASB standards focus on financial materiality, the comprehensive framework of GRI allows for an in-depth understanding of a company’s impact materiality.

UN Global Compact (UNGC)

The UN Global Compact is an initiative launched by the United Nations to encourage companies to adopt sustainable and socially responsible business practices. By joining, companies commit to ten universally recognized principles in the areas of human rights, labor, environment, and anti-corruption, and they pledge to report regularly on their progress.

According to the UNGC online database, 37 of the companies examined have signed the UN Global Compact. By doing so, they have not only committed themselves to the principles of the UNGC, but also to submitting an annual progress report. This demonstrates an ongoing commitment to the UNGC principles at the board and/or management level. In the previous year, 36 companies had signed the UNGC, compared to 28 in 2021.

Sustainable Development Goals (SDGs)

The 17 Sustainable Development Goals (SDGs) are targets for global sustainable development set by the United Nations in 2015 as part of the 2030 Agenda. The SDGs encompass all three dimensions of sustainability (environmental, social, and governance) and cover topics such as poverty alleviation, gender equality, and environmental protection. Although originally not intended as a framework for sustainability reporting, the SDGs now provide companies with a good reference for defining their sustainability goals, setting priorities, as well as measuring and communicating progress. To help companies integrate the SDGs into their sustainability reporting, the UN Global Compact, GRI, and World Business Council for Sustainable Development (WBCSD) developed the SDG Compass.

Of the 47 companies examined, 46 have integrated the SDGs into their sustainability reports. Eight of these companies combine the SDGs with the GRI standards, while 36 align them with both GRI standards and UNGC guidelines. In the previous year, 42 companies had integrated the SDGs, compared to 32 in 2021, indicating growing acceptance and implementation.

CO2 Reporting

A key component of corporate sustainability reporting is the disclosure of CO2 emissions. The most widely used and recognized framework for measuring and reporting greenhouse gas emissions globally is the Greenhouse Gas Protocol (GHG Protocol). The GHG Protocol provides companies with a standardized approach to measuring greenhouse gas emissions, ensuring comparability and transparency. Under the GHG Protocol, a company’s greenhouse gas emissions are divided into three categories: Scope 1 includes direct emissions from company-owned sources, Scope 2 relates to indirect emissions from purchased energy, and Scope 3 encompasses other indirect emissions from the value chain. The following standards relate to measurements according to the GHG Protocol.

Carbon Disclosure Project (CDP)

The Carbon Disclosure Project is a non-profit organization that supports companies in measuring, managing, and reporting their greenhouse gas emissions. Each year, companies are invited to disclose information about their greenhouse gas emissions, climate strategies, and other environmental aspects through questionnaires. The collected data is made publicly available and evaluated in an online database, which is the world’s largest environmental database, evaluating over 21,000 companies. CDP ratings range from A to D in three areas: climate, forests, and water. Companies are rated F if they do not complete the questionnaire or do so inadequately. This study took into account ratings from A to D in the climate area.

As in the previous year, 37 of the companies examined sufficiently completed the CDP questionnaire for 2023. Of these companies, 28 were rated in the A to B range and eight in the C range. One company was rated D. Six companies made it to the annual “A-List 2023” of the CDP, which lists a total of 362 companies worldwide rated A in the climate area. A clear leader is the Swiss fragrance and flavor manufacturer Givaudan, which not only received an A rating in the climate area for the fifth consecutive year but also in the water area. In 2021, 34 companies had validly completed the questionnaire.

Science Based Targets initiative (SBTi)

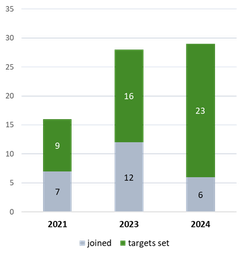

The Science Based Targets initiative is a partnership between CDP, the UN Global Compact, the World Resources Institute, and WWF. It aims to support companies in setting scientifically based emission reduction targets to limit global warming to 1.5°C in line with the Paris Climate Agreement. The Net-Zero Standard introduced in October 2021 also provides companies with a scientifically based framework for setting climate goals with the long-term goal of achieving net-zero emissions. An online database of the SBTi lists companies that have set scientifically based targets or have committed to developing these targets within 24 months of joining. The SBTi is now considered the gold standard and is increasingly being considered by investors.

Of the 47 companies examined, 29 are listed in the SBTi database. Of these, 23 companies have already set clear emission reduction targets, while six companies have joined the SBTi and have yet to develop their targets. In the previous year, only 16 of the 28 listed companies had set emission reduction targets. In 2021, only nine of the 16 listed companies had defined such targets. This development shows that companies are taking their climate responsibility seriously and are increasingly taking concrete steps to reduce emissions.

Number of SMI Expanded companies that have joined the SBTi or have already set emission reduction targets

as part of the SBTi

Converging with Annual Reports

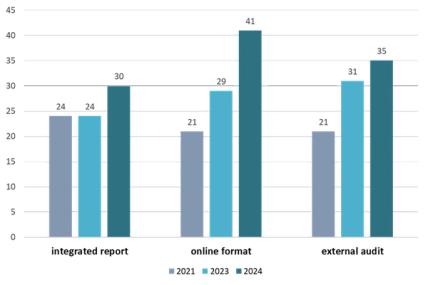

About two-thirds of the companies examined (30) integrate their sustainability report into their annual report. This approach allows companies to combine financial and non-financial aspects in one document, providing a holistic assessment of the company’s performance. In both 2023 and 2021, 24 companies integrated their sustainability report into their annual report.

Of the 30 integrated reports, 27 were presented not only in the traditional PDF format but also in an online format, with important parts of the sustainability report displayed online. Among the 17 standalone sustainability reports, 14 were also presented online. In total, 41 companies chose the online format as a supplement, a significant increase compared to 29 online presentations in 2023 and 21 in 2021. This type of presentation offers several advantages, including linking content through hyperlinks, interactive elements, and better search engine visibility.

External assurance of sustainability reports continues to gain in importance. In 2021, 21 of the companies examined had their sustainability report partially or fully externally audited. This number rose to 31 in 2023 and reached 35 companies in 2024. This trend highlights the growing demand for transparency, credibility, and accountability in sustainability reporting. The trend towards external auditing helps professionalize the entire reporting process and ensures that reported data is reliable.

Number of SMI Expanded companies, that integrated their sustainability report into their annual report, presented parts of their sustainability report online and had their sustainability report externally audited

Sustainability Reporting: Next Steps

The journey towards a sustainable future is an ongoing process that constantly presents new challenges for companies. The findings of this study highlight that sustainability reporting is not just a means of transparency but a strategic tool that significantly contributes to the long-term success of a company. So, what comes next?

Companies should continuously review and develop their sustainability strategies. They should not only meet legal requirements but also proactively pursue innovative approaches to operate more sustainably. Through targeted investments in eco-friendly technologies and the promotion of social justice, companies can strengthen their competitiveness and create real value for society. A crucial step is to firmly embed sustainability in the corporate culture. This requires a shift in mindset at all levels of the company and the involvement of all stakeholders in the sustainability process. Leaders must act as role models and communicate a clear vision.

Moreover, companies should continuously advance their reporting practices and align with best practices and international standards. Utilizing modern technologies and digital platforms can help make reporting more efficient and accessible. By having their sustainability reports externally audited, companies can further enhance their credibility and transparency.

In conclusion, sustainability reporting is far more than just a legal obligation. It offers companies the opportunity to position themselves as responsible actors in a globalized world and actively contribute to addressing the major challenges of our time. Companies that consistently and innovatively follow this path will not only be successful today but also in the future.

About IRF

In recent years, IRF has established itself as one of the leading Swiss consulting firms for economic issues. IRF counts around 40 Swiss and international companies among its regular clients. In addition, IRF has made a name for itself in crisis communication and in accompanying capital market transactions.

Contact

Laura Berkes, Consultant

+41 43 244 81 44

Data Base

| Company | GRI | SASB* | UNGC | SDGs | CDP Climate | SBTi |

|---|---|---|---|---|---|---|

| ABB | Accordance | (x) | x | x | A | Targets set |

| Adecco | Reference | x | x | B | Committed | |

| Alcon | Reference | x | ||||

| ams-OSRAM | Accordance | (x) | x | x | B | |

| Avolta | Accordance | x | x | |||

| Baloise | Accordance | (x) | x | C | ||

| Barry Callebaut | Reference | x | A | Targets set | ||

| Belimo | Accordance | x | x | |||

| BKW | x | x | B- | |||

| Clariant | Accordance | (x) | x | x | B | Targets set |

| Ems-Chemie** | Accordance | x | x | C | Committed | |

| Flughafen Zürich | Accordance | x | x | |||

| Galenica | Accordance | x | C | |||

| Geberit | Accordance | (x) | x | x | C | |

| Georg Fischer | Reference | (x) | x | x | A | Targets set |

| Givaudan | Accordance | x | x | x | A | Targets set |

| Helvetia | Accordance | x | x | B | ||

| Holcim | Accordance | (x) | x | x | A- | Targets set |

| Julius Bär | Reference | (x) | x | A- | Targets set | |

| Kühne + Nagel | Accordance | (x) | x | x | B | Targets set |

| Lindt & Sprüngli | Reference | (x) | x | x | D | Targets set |

| Logitech | Accordance | x | x | x | A- | Targets set |

| Lonza | Accordance | (x) | x | x | B- | Targets set |

| Meyer Burger | Accordance | x | x | |||

| Nestlé | Reference | (x) | x | x | A- | Targets set |

| Novartis | Reference | x | x | x | A- | Targets set |

| Partners Group | Reference | (x) | x | x | C | |

| PSP Swiss Property | x | |||||

| Richemont | Accordance | x | x | x | A- | Targets set |

| Roche | Accordance | x | x | Committed | ||

| Sandoz Group | Reference | (x) | x | x | Committed | |

| Schindler | Reference | (x) | x | x | A | Targets set |

| SGS | Reference | (x) | x | x | A- | Targets set |

| SIG Combibloc | Accordance | x | x | B | Targets set | |

| Sika | Reference | (x) | x | x | C | Targets set |

| Sonova | Accordance | x | x | x | B | Targets set |

| Straumann | Accordance | (x) | x | B | Targets set | |

| Swatch Group | Accordance | x | ||||

| Swiss Life | Accordance | (x) | x | x | B | |

| Swiss Prime Site | Accordance | (x) | x | |||

| Swiss Re | Reference | (x) | x | x | B | Committed |

| Swisscom | Accordance | (x) | x | x | A | Targets set |

| Tecan | Accordance | x | x | C | Targets set | |

| Temenos | Accordance | (x) | x | x | B | Targets set |

| UBS | Accordance | (x) | x | x | A- | |

| VAT Group | Accordance | x | C | |||

| Zurich Insurance Group | Reference | (x) | x | x | A- | Committed |

*(x) indicates companies, that report according to the SASB standards but are not listed in the online database.

**Report from the 2023 financial year not yet published by the end of May 2024, the report from the previous period was taken into account.