Ad hoc publicity and how it is connected to the most expensive TV coverage of the Swiss economy

An information advantage means a lot of money on the stock market. A company must therefore immediately communicate to the outside world when decisions have been made and measures initiated that could move the company's share price beyond the usual market fluctuations. This is where the ad-hoc publicity rules of the Swiss stock exchange come into play. They ensure that all investors can operate on an equal footing.

What do companies have to do to comply with these regulations? It is important that issuers deal with them in depth and know the legal basis. At this point, we would like to refer to the table at the end of this article. It shows impressively what happens when ad hoc rules are violated and fined by SIX Exchange Regulation (SER). It also shows what the "most expensive TV program in the Swiss economy" has to do with ad hoc publicity.

Origin and objectives of ad hoc publicity

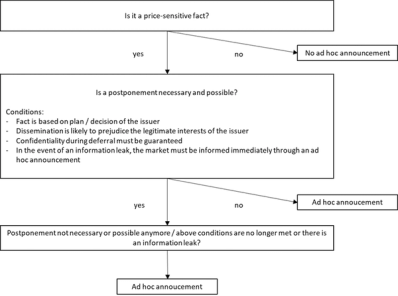

Listed companies mustcomply with many requirements in order tomaintain their listing. These include the duty of ad hoc publicity, which has been enshrined in Art. 53 of the Listing Rules of the Swiss Stock Exchange since 1996. It states that "events that could change the price of a share beyond normal trading fluctuations (price-sensitive fact) must be communicated immediately and clearly by listed companies. This brings all interested market participants to the same level of information." The deferral of this obligation is possible upon cumulative fulfillment of certain conditions and is regulated in Art. 54 of the Listing Rules.

But what is a price-relevant fact? The answer to this question is often not clear. The trigger in each case is a fact that is not yet public and is likely to have a significant impact on the share price when it becomes known. Important: There are no per se facts. Only the publication of annual and interim reports (including quarterly reports) is always subject to ad hoc publicity. Historically, changes in the top management structure, for example, have also been part of this.

SER's website lists possible examples of price-sensitive facts, including mergers, restructurings, purchase offers, CEO changes or changes in the course of business. At the same time, it is emphasized that these need not be price-sensitive per se. Rather, SER recommends that companies ask themselves the following question in each case:

"Would a reasonable market participant be likely to be influenced in his decision to buy, sell or continue to hold the security in question [our company - note IRF] because of the new fact that has not yet been disclosed, believing that the current price inadequately reflects that fact?"

Once the question of price relevance has been answered, this leads to the following decision cascade for the rest of the process:

What does this mean for the listed company's communication?

The issuer is responsible for the timely and correct fulfilment of the ad hoc publication obligation. The regulations relate to form, timing and distribution channels:

| Form | Timing | Channels |

|---|---|---|

| - Media release with clear labelling (flagging): "Ad hoc release pursuant to Art. 53" in all languages - Ad hoc filter function for notifications on the website in all languages | - Publication as soon as the issuer is aware of the main points of the price-sensitive fact - - Outside critical trading hours (90 minutes before the start of trading or after the close of trading) ... - - ... or exceptionally later / during trading hours, if SER is notified by telephone and the facts are transmitted to SER 90 minutes before the planned publication with suspension of trading | - Broad publicity (preferably simultaneously on all channels) - - At least two widely used electronic financial news services (e.g. Bloomberg, Reuters, SIX Financial Information) - - At least two Swiss media of national importance (e.g. NZZ, Tages Anzeiger) - - E-mail distribution list via website registration (push service; link to registration service must be known to SER); each interested party - - Website of the issuer - - SIX Exchange Regulation / Connexor (all languages) |

Figure: Timing Ad-hoc publication (www.ser-ag.com)

All of this requires technology that is geared towards compliance with these rules for the simultaneous distribution of the relevant information on the required sales channels. Specialized service providers such as Interaction Partners take care of this important part (see box at the end of this article).

What happens if the company fails to publish ad hoc news properly before the market opens?

Deciding whether a fact is relevant to the share price is not always easy. Failure to disclose a fact can lead to heavy fines. At the same time, a fact that is falsely disseminated as an ad hoc announcement can also be penalized. This is the case if the ad hoc announcement is misused purely as a marketing tool.

SER may impose a fine of up to CHF 1 million if the ad hoc publicity obligation is breached in terms of form, timing, and addressees. The following table shows that this is not just an empty threat of sanctions.

Figure: SER investigations and fines related to ad hoc obligations (since 2019)

| Date | Issuer | Investigation | Fine in CHF |

|---|---|---|---|

| 15.09.2023 | Walliser Kantonalbank | initiated | |

| 22.08.2023 | Perrot Duval Holding | 25’000 | |

| 03.08.2023 | Airesis | 50’000 | |

| 14.07.2023 | Barry Callebaut | initiated | |

| 13.06.2023 | Relief Therapeutics | 125’000 | |

| 19.05.2023 | Kinarus Therapeutics | initiated | |

| 19.05.2023 | Aevis Victoria | initiated | |

| 12.5.2023 | Perrot Duval | initiated | |

| 21.04.2023 | Leclanché | initiated | |

| 31.03.2023 | Highlight Entertainment | initiated | |

| 17.03.2023 | Orell Füssli | initiated | |

| 27.01.2023 | Alcon | initiated | |

| 12.01.2023 | Clariant | initiated | |

| 06.01.2023 | Swissquote | 75’000 | |

| 22.12.2022 | Airesis | initiated | |

| 07.10.2022 | Spice Private Equity | closed | |

| 25.08.2022 | Interroll | 100’000 | |

| 2.06.2022 | Swissquote | initiated | |

| 24.05.2022 | Poenia | initiated | |

| 1.04.2022 | Spice Private Equity | initiated | |

| 31.08.2021 | U-blox | 25’000 | |

| 10.06.2021 | Relief Therapeutics | initiated | |

| 4.03.2021 | Interroll | initiated | |

| 18.02.2021 | CI Com | 22’000 | |

| 27.11.2020 | Cicor Technologies | closed | |

| 16.10.2020 | Addex Therapeutics | closed | |

| 19.09.2019 | Clariant | 750’000 |

Details of the individual ad hoc publicity procedures and sanctions can be found in the media releases and in more detail (usually anonymized) under Sanctions on the SER website. In most cases, the "time" factor played the decisive role.

Probably the most famous example of an ad hoc fine is the one imposed on Clariant. At CHF 750,000, it is the highest fine for an ad hoc case to date. Roughly summarized, the case involved Clariant announcing the merger agreement with Huntsman Corporation in a media release on 22 May 2017. However, Clariant had already disclosed price-sensitive information to Swiss television on 19 May 2017 with a view to broadcasting a report on the ECO program on the day of the announcement. In the program, the CEO at the time was seen discussing the deal with the Huntsman side at the Widder Hotel in Zurich. However, the merger was not announced until the next day. Due to the fine, this became the most expensive TV report in the history of Swiss business reporting.

Recommendations to fulfill ad hoc regulations

In ad hoc considerations, the behavior of market participants can never be predicted with absolute certainty and, where work is done, mistakes happen. This makes it even more important for the issuer to be well prepared. Our recommendations:

1. familiarize yourself with the subject matter

Even if the initial decision regarding price relevance is discretionary, SIX has clear regulations and guidelines for the subsequent processes. It is important to read and internalize these and to actively monitor changes.

2. define responsibilities from the outset

A team and clear responsibilities must be defined for ad hoc publicity throughout the entire process and decision tree. The top management should be involved.

3. select partners carefully

As ad hoc publicity obligations do not normally occur frequently in a company, it is worth working with partners who are familiar with the subject matter. A partner with the highest possible success rate is also needed for the technical solution of the dispatch.

4. have a plan B ready

Expect the unexpected! Even the best technology and the best people can fail. These scenarios need to be factored in and a plan B prepared accordingly. This applies not only to sending the media release and publishing it on the website, but also to uploading it to the Connexor platform. E.g., what to do if the login suddenly stops working?

***

The technical solution, Kilian Maier, CEO Interaction Partners

Ad-hoc: Why this is a good use case for standard software

Ad hoc message distribution is a great fit for niche off-the-shelf software and automated integrations with third-party applications.

Here are the reasons:

Clear rules - perfect for software

As described above, it can be unclear whether a message qualifies as ad hoc or not. However, once the decision has been made, the process is clear. The news requires an ad hoc flag (language-dependent), which must be displayed in e-mails and on the homepage. Ad hoc also requires an additional distribution list (national and international news agencies, media). In addition, new subscribers must be added to the correct lists and people who unsubscribe must be reliably unsubscribed. All of this can be fully automated, and if properly programmed, tested and maintained, a machine will do the job better, faster and more consistently than a human ever could.

Data consistency - "single source of truth"

Ad-hoc messages must be distributed at least to SIX, the e-mail distribution list, the additional ad-hoc distribution list and the issuer's homepage. If necessary, the issuer may also aim for broader distribution via an international newswire. To do this, the news must be inserted separately into the various systems (copy and paste). Such a process is very error-prone, especially if the text is changed at the last minute, perhaps even in several languages. However, if the issuer works with a specialized provider such as schedulR, which has connected the various systems, there is a "single source of truth" and this is distributed digitally to all channels via proven and resilient interfaces.

Speed is critical

Time is a decisive factor when publishing an ad hoc announcement. Thanks to specialized software and established interfaces, the process is very fast. Newswires and the homepage are served within 2 minutes and most e-mails (> 95 %, often almost 99 %) are also delivered within this time.